Health in Japan

Understanding Shakai Hoken, Kokumin Hoken, and the Crisis of Having Neither

LIFE IN JAPAN

1/22/20264 min read

The Japanese healthcare system is considered one of the best in the world, but the reality for foreigners can be a maze. The coverage you have—or lack thereof—completely defines your access to doctors, the cost of appointments, and your financial risk in an emergency.

This Manual do Japão guide clearly explains the three distinct realities: that of the formal worker with Shakai Hoken, the freelancer/student with Kokumin Hoken, and the dangerous situation of having no insurance. Understanding this is the first step to protecting your health and your wallet in Japan.

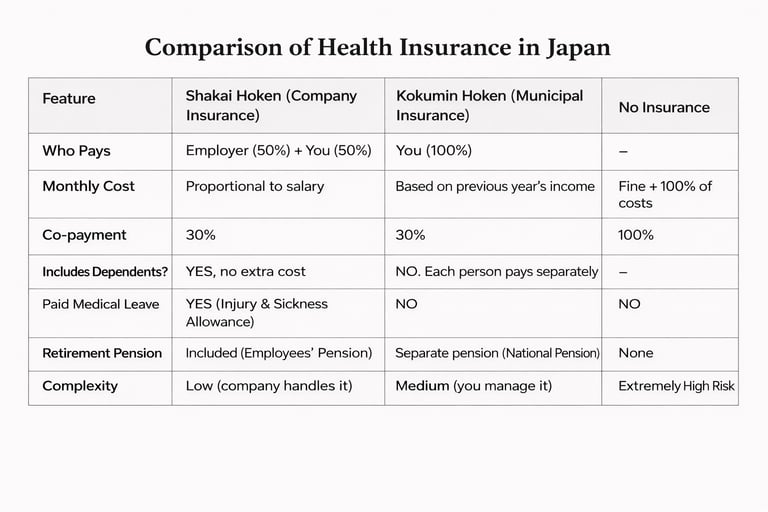

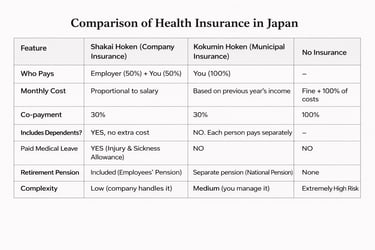

1. Shakai Hoken (社会保险): The "Corporate Health Plan" (The Most Complete)

Who has it: Workers at companies under the Japanese CLT regime (正社員 - Seishain) and, in many cases, long-term contract workers (契約社員). Enrollment is mandatory for the company.

How it works: It is insurance split between you and your employer. The company pays about 50% of the total cost. The deduction from your salary is automatic.

Main Coverage:

Appointments and Hospitalizations: You pay only 30% of the total cost (自己負担 - Jiko futan).

Medications: Only 30% of the price at pharmacies.

Paid Sick Leave: In case of prolonged absence due to illness, you receive a subsidy (傷病手当 - Shōbyō teate).

Pension and Unemployment: The package includes a pension (年金 - Nenkin) and unemployment insurance.

Key Advantage: Your direct dependents (spouse, children) can be included in your insurance at no extra cost, and they also pay only 30% of treatments.

Disadvantage: The salary deduction is high, especially if you have a high income.

2. Kokumin Hoken (国民健康保険): The "Municipal Health Plan"

Who has it: Freelancers, students, unemployed individuals, or workers at companies that do not offer Shakai Hoken (like some hakken/temp agencies). It is your responsibility to enroll.

How it works: It is an individual and municipal insurance. You register at the city hall (区役所/市役所) and the cost is calculated based on your declared income from the previous year.

Cost: Can vary drastically. In the first year, with no income history in Japan, you will pay a standard rate (which can be high, e.g., ¥15,000-¥20,000/month). The following year, if your income is low, it may drop to ¥3,000-¥5,000. If it is high, it can rise significantly.

Coverage: Like Shakai Hoken, it covers 70% of medical costs. You pay 30%.

Major Disadvantage: It does NOT automatically include paid sick leave or dependents. Each family member needs a separate policy, paying individual rates. For a family, the total cost can be much higher than Shakai Hoken.

3. No Insurance: The Maximum Danger Zone

Who are they: People in an irregular situation, some students who ignore the obligation, or workers who became unemployed and did not transfer to Kokumin Hoken.

The Harsh Reality:

Total Cost: You pay 100% of everything: appointment, exams, medication, hospitalization.

Prohibitive Prices: A simple visit to a general practitioner can cost ¥10,000. An emergency with an ambulance and some tests can easily exceed ¥100,000. Childbirth can cost over ¥500,000.

Refusal of Service: Some private clinics or hospitals may refuse to treat those without insurance.

Fines and Legal Problems: Not having health insurance is illegal. The city hall can calculate your retroactive contributions and charge fines. Renewing your visa without being up to date with insurance is practically impossible.

The Only Exception (Attention!): In case of a serious accident or sudden life-threatening illness, the hospital is obligated to provide emergency care first. But the astronomical bill will come later, potentially leading to lawsuits and deportation.

Quick Comparison Table

Special Situations and Crucial Tips

Hakken/Contractor Worker: CONFIRM if the company is deducting and providing Shakai Hoken. Many do not, and the responsibility to enroll in Kokumin Hoken is YOURS.

Lost Your Job (with Shakai Hoken): You have a deadline to transfer to Kokumin Hoken. The city hall will issue a new card. DO NOT BE UNCOVERED.

Student: It is mandatory to have Kokumin Hoken. Many schools help with enrollment. The cost is usually very low (Exemption/Reduction - 減額 - Men'gaku).

Very Low Income: With Kokumin Hoken, you can apply for a reduction or exemption (免除 - Menjo) at the city hall. Don't fail to ask!

Golden Tip: If you are unsure, go to the Health Insurance Desk (健康保険課 - Kenkō Hokenka) at your city hall and explain your situation. They will guide you.

Action Checklist: Which Case is Yours?

Do you work for a Japanese company? → You have Shakai Hoken. Keep your card safe.

Are you a student, freelancer, or work for an agency? → You MUST have Kokumin Hoken. Go to the city hall.

Don't have a physical insurance card? → You are in the danger zone. Resolve this TODAY.

Have family in Japan? → If you have Shakai Hoken, register them as dependents. If you have Kokumin, each one needs insurance.

Conclusion: Insurance is Not an Option, It's an Obligation

In Japan, not having health insurance is a financial and legal time bomb. The choice is not between having it or not, but between planning within the system or being caught off guard by a bill that can destroy years of savings.

Shakai Hoken is the ideal scenario. Kokumin Hoken is the viable and mandatory path for those not in the corporate system. Having neither is a direct route to loss and serious problems with immigration.

Take care of your bureaucratic health so that when you need it, you can take care of your physical health with peace of mind.

#SaudeNoJapao #ShakaiHoken #KokuminHoken #SeguroSaudeJapao #BrasileirosNoJapao #ManualDoJapao #VidaNoJapao #DireitosTrabalhistasJapao #PrevidenciaJapao #KenkoHoken